Insights

Should NZX Directors Own the Companies They Govern?

Published May 2026

Author:

ANALYSIS: Companies need to formalise skin in the game and make transparent minimum shareholding requirements

It has been a tough few years for investors in equities on the NZX. The five-year annualised return of the S&P/NZX 50 Gross Index stood at a measly 0.3% as at 30 April 2026, and almost half the members of the index have posted negative cumulative total returns over that period. Naturally, this has sharpened investor scrutiny of governance practices. While local economic conditions and global geopolitical issues can legitimately be blamed for some of the poor performance, at least some company boards will have faced tough questions at recent shareholder meetings.

Fletcher Building (-49%), Synlait Milk (-87%) and Ryman Healthcare (-82%) are all examples of NZX companies that have seen significant destruction of shareholder value over the last five years1, followed by deep governance resets, which has included substantial board renewal.

The principal-agent problem is fundamental to economics and describes a situation investors know well: the conflicts that can arise between a company’s owners and its managers. That is where the board of directors comes in. Shareholders select qualified candidates to represent their interests and monitor the activities of management.

If one of the roles of the board is to represent the interests of investors, should directors themselves be required to be shareholders in the business? Not necessarily in New Zealand. Our analysis finds that only a handful of the largest NZX companies require non-executive directors (NEDs) to hold a certain level of shares, with a further handful encouraging a minimum holding.

Around half of the 50 largest NZX companies have no publicly disclosed policy, nor encouragement, for NEDs to hold shares. We are focused on non-executive directors because executive directors are more likely to already hold shares either directly or through executive remuneration plans.

Other people's money

Concern underlying the agency problem goes back at least as far as Adam Smith’s The Wealth of Nations in 1776. Writing on the topic of joint-stock companies, a forerunner of the modern company, Smith observed:

“The directors of such companies, however, being the managers rather of other people’s money than of their own, it cannot well be expected, that they should watch over it with the same anxious vigilance…”2

In other words, managers without “skin in the game” cannot necessarily be expected to exercise the same care and attention as a company’s shareholders and owners.

Academic literature sets out the roles of a board of directors relatively clearly: to monitor and supervise the executive, while also providing an accountability mechanism to shareholders. The board appoints the CEO; shareholders appoint the board. Boards are not only backward-looking, of course. They also play an essential role in strategy formulation and policy making3.

Director share ownership is not just symbolic, it helps align directors with shareholders, making sure they are also ‘at risk’ for poor decisions and encourage thinking long-term about capital allocation, risk, remuneration and strategy.

Our analysis

For our analysis, we reviewed the public disclosures of NZX 50 companies. We do not claim the analysis is perfect, and there is certainly some subjectivity in the results. It is based on publicly available disclosures so will not capture internal policies. Nevertheless, we think the findings are interesting and indicative of broader trends.

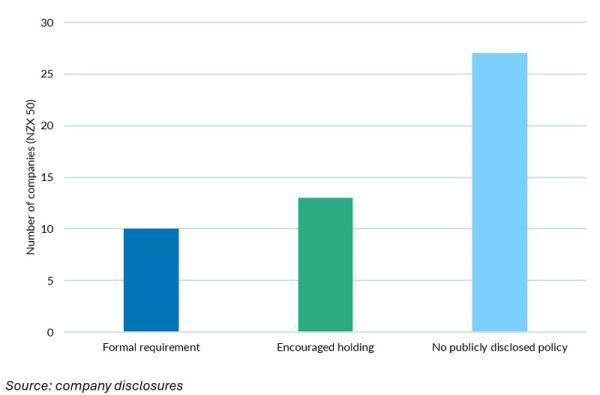

We found that ten NZX companies have some form of formal requirement for NEDs to hold shares in the company, while a further 13 encourage NEDs to own shares. Among these 23 companies, there were various combinations of minimum holding amounts and time horizons over which NEDs were expected to build their shareholdings.

Findings from our analysis of company disclosure on director shareholding requirement

Here are some examples that stood out to us. There were many other good examples, but we have selected a few to illustrate the different approaches:

Auckland International Airport requires directors to use at least 15% of their net fixed base annual director fee each year for three years to acquire shares, until their holding is at least equivalent to one net fixed base annual fee.

Ryman Healthcare introduced a formal requirement in 2023 as part of its closely watched governance reforms. The policy requires NEDs to hold a minimum shareholding equivalent to the value of their base director fee within the first five years of appointment. NBR reported on a flurry of share buying by Ryman NEDs in August last year.

Contact Energy “encourages” directors to hold at least 20,000 shares within three years of appointment, subject to personal circumstances. At the current share price, this would be close to $200,000 in value.

Another approach is taken by NZX Limited, which has a formal share purchase plan requirement tied to director remuneration. NZX directors must use a portion of their fees to buy shares in the company: 50% of the Chair fee above $100,000, and 50% of Director fees above $50,000, unless they are not permitted to do so for compliance or other reasons.

From our perspective, whether the expectation is framed as a formal requirement or an encouragement is less important than whether it is written down in policy. A disclosed policy sets a strong expectation that NEDs will hold shares in the companies they serve, subject, of course, to appropriate exceptions.

Director ownership is not always straightforward

An essential attribute of a NED is independence. A majority-independent board is generally a preference among investors globally, including ourselves. There is certainly a level of share ownership at which a director is no longer independent, therefore, some may argue that it is acceptable for NEDs not to hold any shares. We disagree and we think most minority investors would hold this position. Our view is that there is a level of share ownership that aligns NEDs with long-term shareholders while still preserving their independence.

Another concern is that share ownership could heighten focus on short-term share price performance rather than long-term value creation. Further, we do not want to see a situation where an otherwise qualified and suitable candidate is unable to become a director because they cannot purchase the minimum required number of shares due to personal circumstances. If this leads to boards that have less diversity of thought and opinion, we believe this would also be a suboptimal outcome for shareholders.

Skin in the game

As investors, we look to boards to keep management accountable and make decisions for the long-term benefit of the company. In our view, it is reasonable for long-term shareholders to expect NEDs to have some economic exposure to the companies they oversee, subject to appropriate exceptions.

We think this expectation should be made clear to potential directors, either through a formal policy requirement or a publicly disclosed expectation.

As discussed earlier, one part of Ryman’s deep governance reset was the introduction of a formal minimum shareholding requirement for NEDs, seen as a step in rebuilding investor confidence.

Infratil, which has been a bright spot on the NZX, providing investors around +100% total return4 over the last five years, encourages directors to acquire and hold shares in its Board Charter.

Infratil insiders, including several NEDs, were notably buying up the stock last year, a signal to shareholders of confidence in the future of the company.

Investors can already see in company annual reports whether directors hold shares. The next step is for more companies to make clear whether they expect their directors to do so.

1Cumulative Total return for the five years to 30 April

2Adam Smith, An Inquiry into the Nature and Causes of the Wealth of Nations (1776), Book V, Chapter I, Part III, Article I.

3Definition from Hilmer, F. G., & Tricker, R. I. (1991) Directors and Boards: Their Role and Structure

4Cumulative Total return for the five years to 30 April

Disclaimer: This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. This article does not contain financial advice. Some of the Octagon portfolios may own securities issued by companies mentioned in this article.

Octagon Asset Management is the investment manager for Octagon Investment Funds and the Summer KiwiSaver scheme.

Filter insights

Related reading

It is never easy to know when a boom has gone too far. But that is usually when things become most interesting.

Few parts of th…

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

It is no secret that us New Zealanders love to invest in property as a way of building wealth. …

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

For investors that hold assets denominated in a foreign currency, there is a direct exposure…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatil…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…