Insights

Datacentres and the new capital cycle

Published April 2026

If AI is the new industrial revolution, datacentres are the factories.

It is never easy to know when a boom has gone too far. But that is usually when things become most interesting.

Few parts of the market capture that tension better than datacentres. The sector sits at the intersection of AI enthusiasm, hyperscaler capex, debt markets, energy and real estate. The bull case is easy to see: structural demand growth, long contracts, high-quality counterparties, scarce power and exceptional development economics.

The harder question is whether all of this investment will ultimately earn an adequate return.

From what we can see, debt and equity capital is flowing freely into the sector, leverage is high and development returns can look extraordinary. Yet datacentre investors are still underwriting a future in which AI services can be properly monetised and efficiency gains do not hollow out the need for so much physical infrastructure.

Why the assets look so attractive

Datacentres are often lumped in with real estate. That is too simplistic.

A modern AI-oriented datacentre is less like a passive warehouse and more like a piece of industrial infrastructure. The value is not in the building. It sits in location, grid connection, power access, cooling systems, connectivity, approvals, engineering capability and tenant covenant.

Developer management teams point to initial yields on a powered shell of roughly 7–8%, and into the double digits for more fitted product. There is limited transactional evidence, but the collective wisdom in the industry suggests these assets could trade at stabilised cap rates of around 6%. Put simply, developing at 10% yields and exiting at 6% yields implies a 67% development margin. Even a powered shell at 8% would deliver a margin above 30%, at the top end of the roughly 15–30% achieved across conventional real estate sectors.

The attractiveness is reinforced by contractual structure. These are typically long-dated leases with embedded income growth, backed by counterparties that at the top end of the market are among the largest and most profitable companies of our time.

This is also why analysts approach the sector from different angles: technology, infrastructure and property. Each lens has merit, which is part of what makes the sector so interesting.

A Google data centre in the Netherlands

The perfect asset class for other people’s money

From the perspective of infrastructure fund managers, datacentres are close to ideal.

They offer long-term growth, very large deal sizes, substantial leverage, and assets that can absorb extraordinary amounts of fee-generating capital. If you were designing an asset class to suit the modern infrastructure fund, you would probably end up with something very similar.

The transactional evidence tells the same story. Blackstone’s 2024 acquisition of AirTrunk at an implied enterprise value of more than A$24 billion, or roughly 21 times contracted EBITDA, was one of the clearest signs yet that private capital is willing to pay up for large-scale digital infrastructure.

A consortium including IFM acquired Switch in 2022 in an approximately US$11 billion transaction including debt. More recently, SoftBank was reported to have undertaken due diligence on the operator, with owners seeking a valuation of around US$50 billion including debt, although those discussions appear to have stalled.

Closer to home, Canberra Data Centres has become Infratil’s largest investment and, on latest disclosure, its independent valuation increased to A$15.0 billion as at 31 March 2026. Infratil’s last reported IRR on the investment, as at 30 September 2025 after roughly nine years of ownership, was 36.4% per annum. As you can imagine, the performance fees for the asset managers are eye-watering.

The money keeps flowing. The problem is that when an asset class becomes this attractive, it rarely stays mispriced for long. The medium-term risk is not a lack of capital, but so much new capital that the handsome returns currently on offer are competed away.

A map of the CDC data centres in Australia and New Zealand

Componentry and power the key constraints

One of the more interesting developments in recent weeks highlights industrial inputs and power as the limiting factors.

A recent Bloomberg report noted that almost half of US datacentres planned for this year are expected to be delayed or cancelled. The reason was not weak demand, but shortages of transformers, switchgear and batteries, with lead times in some cases blowing out to five years.

Those same inputs are needed not only for AI-related power demand, but also for broader grid build-out as electricity consumption rises with electric vehicles, heat pumps and air-conditioning systems.

Another constraint is the regulatory process required to secure grid access. Regulated monopolies tend to control these networks and act as gatekeepers to new connections. Their upstream transmission infrastructure must be capable of handling the large and concentrated power requirements of the datacentre operator. In key locations, transmission capacity is limited, while network expansion operates on far longer timeframes than the roughly 18-month datacentre construction period.

Monetisation is the question

The sceptical case on AI infrastructure is not whether sufficient demand exists. It is that the economics remain unsettled.

The issue is not whether AI will prove transformative. It almost certainly will. The issue, as in earlier capex booms, is whether the recent investment will be successfully monetised. This is fundamental to the datacentre value equation. If these “AI factories” do not generate enough future revenue for end customers, what happens at the end of the initial lease term?

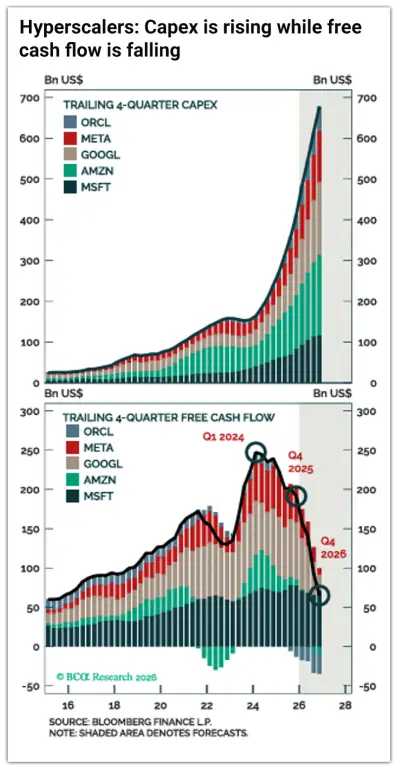

In a recent note, BCA drew parallels with the emergence of the internet and the subsequent boom in telecoms infrastructure spending. Since 2000, internet traffic volumes have risen by half a million percent, equivalent to 42% per annum. Despite that, capex on internet hardware has fallen dramatically. The five largest US telecom companies collectively spent US$71 billion in capex through 2025. That compares with US$600 billion in total compute spend signalled by OpenAI alone through to 2030.

Even though the technology was transformative and widely adopted, telecoms investment never recovered to the lofty highs of the early 2000s. Ultimately, the revenue streams were not large enough to support investment at that scale.

AI may be transformational at an economy-wide level yet still fail to deliver commercial success for the companies funding the build-out.

Meanwhile, hyperscaler capex is expected to rise to US$678 billion this year, up roughly 64% from US$412 billion in 2025. The profits needed to justify that are enormous.

Why this time may be different

And yet this cycle has clear differences from the dotcom capex bust.

Speculative investment was rampant during the fibre build-out of the internet boom. That led to overcapacity, collapsed pricing, low returns on capital, debt defaults and eventual sector consolidation.

This wave of investment is being underwritten by companies with extraordinary balance sheets, cash generation and clear visibility into demand. The MAG7 are not investing speculatively in the way earlier-cycle participants did. They are responding to real usage growth and, in some cases, staking management credibility on the idea that demand broadens from model access into coding tools, workflow automation, advertising optimisation and agentic use cases.

There is evidence of that already. On its February earnings call, Block said it planned to reduce headcount by 40%, from around 10,000 to fewer than 6,000, while leaning into AI-based tools that enabled more productive ways of working. WiseTech Global likewise said at its February result that it was moving to an AI-led operating model and planned to reduce headcount in some teams by up to 50%.

It is hard to believe the firms at the frontier of AI will not find a way to monetise these economics.

What to watch from here

· Monetisation: Are AI services starting to earn enough revenue and margin to justify the scale of infrastructure spending? Or are investors still underwriting future pricing power and efficiency gains?

· Power and equipment: Watch the availability of transformers, switchgear, batteries and grid access. If those remain constrained, they may shape deployment as much as demand does.

· Capital discipline: As more infrastructure capital floods into the space, keep an eye on whether returns on cost and stabilised valuations begin to compress. That is the classic capital-cycle risk.

· Counterparty quality: The economics look very different depending on whether the tenant is a hyperscaler, a government customer, a major enterprise or a more leveraged AI intermediary. Covenant still matters.

· Obsolescence and efficiency: What happens if models become much more efficient, rack density rises faster than expected, or certain asset types prove less adaptable than the market assumes? That risk goes directly to terminal value.

Bottom line

Datacentres are not just another property theme, and they are not simply a proxy for AI hype.

They are where abstract enthusiasm about AI becomes concrete spending on land, power, chips, concrete and steel. That is why the sector has attracted so much capital, and why valuations have surged. The attraction is obvious: long-duration growth, strong counterparties, leverage and scale. The risk is equally obvious: capital floods in, bottlenecks move upstream, AI gets cheaper and more efficient, and some of today’s exceptional economics are competed away.

You do not need to believe the AI story is a mirage to be cautious here.

Tobias Newton is an equity analyst for Octagon Asset Management.

This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. This article does not contain financial advice. Some of the Octagon portfolios may own securities issued by companies mentioned in this article.

Octagon Asset Management is the investment manager for Octagon Investment Funds and the Summer KiwiSaver scheme.

Filter insights

Related reading

It has been a tough few years for investors in equities on the NZX. The five-year annuali…

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

It is no secret that us New Zealanders love to invest in property as a way of building wealth. …

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

For investors that hold assets denominated in a foreign currency, there is a direct exposure…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatil…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…