Quarterly Market Comment

As an active fund manager, Octagon Asset Management prioritises high-quality research as an input to decision making. It draws on research from a range of sources, local and global. This includes research provided by Forsyth Barr. Below is its most recent Quarterly Market Comment.

Quarterly Market Comment

For the quarter ended 31 March 2026

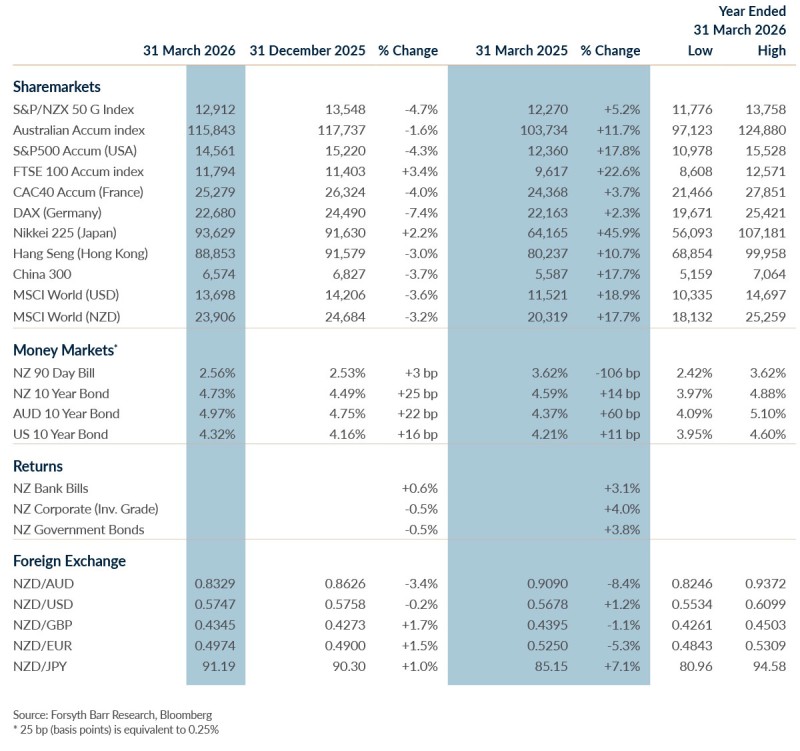

- The past three months have seen the MSCI World Index fall -3.6% in US dollar terms, in large part driven by a tough month in March following the escalating military conflict in the Middle East. Returns in New Zealand dollars were slightly better, but still -3.2%.

- Market performance across regions over the quarter was broadly negative to relatively flat. The US S&P 500 index fell -4.3% in local terms, while UK and Japanese markets eked out small gains. NZ equities declined -4.7%; Australian equities were -1.6% lower over the quarter.

- Fixed income returns were impacted by growing inflation concerns, pressuring yields higher and bond prices lower over the quarter. NZ investment-grade corporate bonds fell -0.5% for the quarter.

Middle East conflict delivers a tough March

Geopolitical tensions were the main driver of markets in March, with conflict between the US, Israel, and Iran increasing uncertainty and weighing on market sentiment. While the focus here is on financial impacts, it is important to acknowledge the human cost of any military action. At the time of writing, a tentative ceasefire has been agreed, offering some hope for de-escalation.

Even before the conflict broke out in March, markets were facing a more challenging backdrop. Concerns had been building around elevated valuations in parts of the technology sector, alongside a more cautious reassessment of how quickly artificial intelligence (AI) would translate into tangible results, softening equity returns in some parts of the market.

The conflict in Iran quickly translated into tangible economic consequences—most notably through disruptions to global energy supply. The closure of the Strait of Hormuz, a critical artery for global trade, has been central to market concerns. The Strait facilitates roughly 20% of global oil shipments, alongside a meaningful share of natural gas and other key commodities. As a result, oil prices rose sharply—from around US$70 per barrel to trading as high as around US$120—with gas prices also increasing materially.

These higher energy costs are now flowing through to the broader economy. Fuel and transport costs have risen, and many goods and services are becoming more expensive. Airlines have increased ticket prices, shipping costs have climbed, and businesses are starting to pass on higher input costs to customers. Disruptions have also affected related industries such as chemicals and fertilisers, adding to overall inflation pressures.

Equity markets have responded negatively, reflecting concerns that prolonged disruption could keep energy prices elevated. This raises the risk of both higher inflation and slower global growth.

Encouragingly, there have been early signs that an end to the fighting may be approaching, although uncertainty remains around what operations through the Strait will look like even if/when some form of de-escalation occurs.

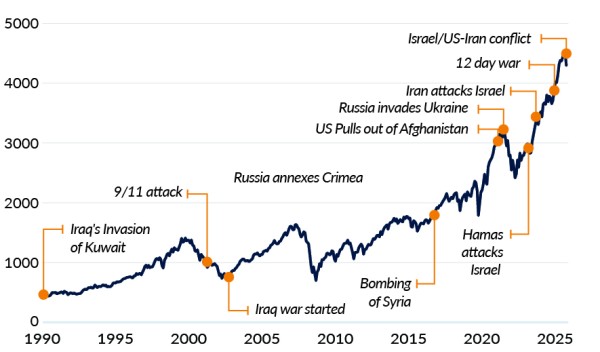

MSCI world index and geopolitical events

Source: Refinitiv, Forsyth Barr analysis

Volatility and the role of sentiment

Recent market movements have been driven largely by fast-changing news, highlighting how quickly sentiment can move markets in the short term. Daily updates—ranging from military developments to progress in negotiations—have led to increased volatility.

If disruptions to key global trade routes persist, the impact on inflation and economic growth could be more lasting. However, history shows that markets and businesses often adapt more quickly than expected. Supply chains adjust, companies respond, and over time, underlying economic fundamentals tend to reassert themselves.

Artificial intelligence: a rapidly evolving landscape

While global events have been driving markets in the short term, artificial intelligence (AI) remains an important longer-term trend.

AI is advancing quickly. The technology is improving, becoming cheaper, and being used more widely across different industries. This is creating opportunities for businesses to work more efficiently, reduce costs, and develop new sources of revenue.

Markets are now moving into a more selective phase. Earlier excitement is giving way to a greater focus on companies that can actually turn AI into real profits—those with strong competitive positions and clear ways to make money from the technology.

At the same time, the risks are becoming clearer. The pace of change is fast, competition is increasing, and the level of investment required is high. Not all companies will benefit, and some may come under pressure as it becomes easier for new competitors to enter the market.

Periods of major technological change have historically brought both disruption and opportunity. While outcomes will differ across companies, the overall opportunity is growing.

Interest rates moving higher with bond yields improving

Recent global tensions have pushed energy prices higher, which is lifting the cost of living. These increases are starting to flow through to other areas, including transport, food, and everyday goods.

This has made things more complicated for central banks. While interest rates were previously expected to remain relatively steady before moving gradually higher, there is a growing sense that interest rates may rise quicker than previously thought, especially if cost pressures don’t ease.

As a result, bond yields have risen since the start of the year, offering improved income. At the same time, bonds continue to provide some protection during more acute periods of market fluctuations.

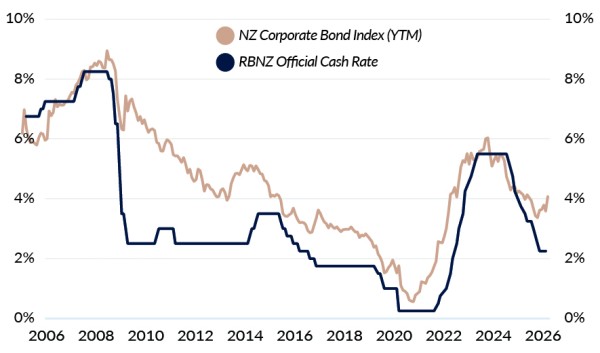

NZ corporate bond index (yield-to-maturity) and RBNZ official cash rate

Source: Bloomberg, ANZ, Forsyth Barr analysis

A steady approach through uncertain times

The past quarter has been a reminder that ups and downs are a normal part of investing. Global events, rising costs, and changing expectations can all create periods of uncertainty.

In times like this, markets can react quickly to new information and sometimes move more than they should in the short term. Over time, however, what really matters are the basics—how companies earn money, grow, and generate cash. Markets tend to settle and reflect these fundamentals in the long run.

Responding to short-term market moves is often counterproductive. A well diversified portfolio, combined with a disciplined long-term approach, remains the most effective way to navigate these environments.

Matt Henry

Head of Wealth Management Research

Zoe Wallis

Investment Strategist

Not personalised financial advice: The recommendations and opinions in this publication do not take into account your personal financial situation or investment goals. The financial products referred to in this publication may not be suitable for you. If you wish to receive personalised financial advice, please contact your Forsyth Barr Investment Adviser. The value of financial products may go up and down and investors may not get back the full (or any) amount invested. Past performance is not necessarily indicative of future performance.

Disclosure: Forsyth Barr Limited and its related companies (and their respective directors, officers, agents and employees) (“Forsyth Barr”) may have long or short positions or otherwise have interests in the financial products referred to in this publication, and may be directors or officers of, and/or provide (or be intending to provide) investment banking or other services to, the issuer of those financial products (and may receive fees for so acting). Forsyth Barr is not a registered bank within the meaning of the Reserve Bank of New Zealand Act 1989. Forsyth Barr may buy or sell financial products as principal or agent, and in doing so may undertake transactions that are not consistent with any recommendations contained in this publication. Forsyth Barr confirms no inducement has been accepted from the researched entity, whether pecuniary or otherwise, in connection with making any recommendation contained in this publication.

Analyst Disclosure Statement: In preparing this publication the analyst(s) may or may not have a threshold interest in the financial products referred to in this publication. For these purposes a threshold interest is defined as being a holder of more than $50,000 in value or 1% of the financial products on issue, whichever is the lesser. In preparing this publication, non-financial assistance (for example, access to staff or information) may have been provided by the entity being researched.

Disclaimer: This publication has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. However, that information has not been independently verified or investigated by Forsyth Barr. Forsyth Barr does not make any representation or warranty (express or implied) that the information in this publication is accurate or complete, and, to the maximum extent permitted by law, excludes and disclaims any liability (including in negligence) for any loss which may be incurred by any person acting or relying upon any information, analysis, opinion or recommendation in this publication. Forsyth Barr does not undertake to keep current this publication; any opinions or recommendations may change without notice. Any analyses or valuations will typically be based on numerous assumptions; different assumptions may yield materially different results. Nothing in this publication should be construed as a solicitation to buy or sell any financial product, or to engage in or refrain from doing so, or to engage in any other transaction. Other Forsyth Barr business units may hold views different from those in this publication; any such views will generally not be brought to your attention. This publication is not intended to be distributed or made available to any person in any jurisdiction where doing so would constitute a breach of any applicable laws or regulations or would subject Forsyth Barr to any registration or licensing requirement within such jurisdiction.

Terms of use: Copyright Forsyth Barr Limited. You may not redistribute, copy, revise, amend, create a derivative work from, extract data from, or otherwise commercially exploit this publication in any way. By accessing this publication via an electronic platform, you agree that the platform provider may provide Forsyth Barr with information on your readership of the publications available through that platform.