Insights

Volatility ‘built in’ to investment markets

Published August 2022

Author:

ANALYSIS: No-one likes to forecast a recession, which is odd.

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatility: ‘what you see is all there is’ (WYSIATI).

Volatility in this sense refers to the general level of price movement in asset prices.

We all know markets are forward-looking, and that forecasting the future is hard. What we have in front of us – our research, experience, models, and understanding of how things ‘usually’ interrelate – is all there is. After that, we are simply reaching for things that aren’t there.

Sometimes our reaching is based on strong mean-reverting characteristics of free markets or societal preferences, other times we are applying probabilities to an enormous range of plausible outcomes.

Every investor does this in their own way. Many different views of the future creates an inherent level of volatility.

In Thinking Fast and Slow we are told we can improve our forecasting outcomes if we take the time to be disciplined and apply logic. When we look at the possible outcomes, this discipline and logic should stop us taking short cuts and joining dots that don’t belong together.

It is very hard to do, and the book refers to many experiments in which very smart people made similar mistakes, based on our ‘hard wiring’ that allows us to reach decisions quickly. Quick decisions help us navigate life in a very complicated society.

Thinking Fast and Slow by Daniel Kahneman.

In reading the book, I often wanted to make the easy decision for me to reach based on my own experience and understanding –rather than stepping back and looking for other solutions or other relationships that might exist, or flaws in the first solution that came to hand. To me, that’s the whole point of the book: it takes forceful effort to pause and look at a problem from multiple standpoints.

Which brings me to the sub title of this article: no-one likes to forecast a recession. I find this quite odd.

If we use a discounted cashflow analysis for a security, usually a listed company, 60% or more of that company’s valuation depends on what happens in the company’s life after 10 years from today. It is almost inevitable that, over that time period, we will experience a recession.

That recession will hardly affect that long-term valuation at all – unless the company happens to have too much debt at the time, or the cause of the recession simply sees trading stop, for example, during a pandemic.

For most companies, it is far more important to understand the competitive and regulatory backdrop – how the company adapts to change, and the way it spends its cash – to determine long-term value.

Why and how?

So why do company share prices exhibit high volatility, dependent on where we are in this economic cycle?

How can the same company have a stock market valuation that implies a price to earnings ratio (PE) of 15x some high short-term future earnings number, and then 8x some much lower future earnings number?

The long-term valuation in the discounted cashflow analysis already captures cycles and (hopefully) uses long-term margin and return on capital assumptions in the outer years, guided by an extremely long-term history of similar successful companies.

We all have the information about where the cycle and stock prices are every day, but the market appears to be being driven by lots of people extrapolating current conditions – the desire to get ‘in’ when markets are rising even when stock prices imply a version of the future that is likely to have a low probability of eventuating.

Then, the same desire to get ‘out’ when prices are falling to avoid short term losses, driving prices to low levels, that also imply a version of the future that has a low probability attached.

This is built in volatility; not only can’t we accurately predict the future (which is inherently volatile), we amplify it by taking shortcuts in our investment thinking that allows us to take share prices to points where they reflect very low probability long-term outcomes.

Today’s investment backdrop

Thinking about today’s investment backdrop, in recent weeks we have seen signs the bond market is expecting a recession – by lowering longer-term interest rates well below where many nation’s central banks have forecast them to be to ensure inflation comes down. At the same time, the earnings forecasts for sharemarkets have hardly budged, partly shielded by upgrades to earnings for oil and gas companies.

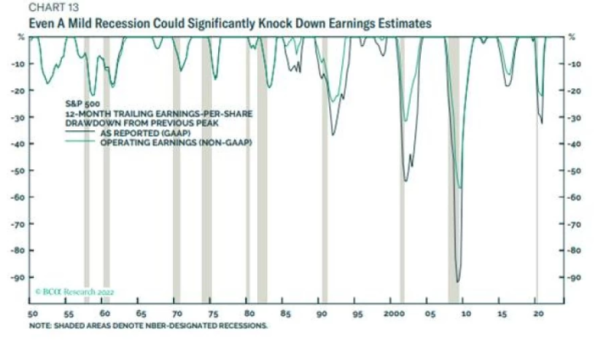

The below chart from global research house BCA shows what happens to actual reported earnings for stocks listed on the US S&P500 when a recession (or even an economic slowdown) hits.

Source: BCA Research.

WYSIATI. We (as a market) see an increasing chance of a recession, but we don’t factor it into earnings forecasts, despite the 70 years of compelling evidence in this chart.

Has the equity market thought ‘fast’ and extrapolated current earnings, rather than ‘slow’ and logically considered what happens to earnings in a recession?

If a recession doesn’t happen, we will see volatility in the bond market.

If a recession does happen, we will see volatility in the equity market.

We are talking the future here, so there is a plausible outcome that says both markets are right – it just seems like that is a low-probability outcome based on the information we have.

In all three future outcomes, the long-term valuation of most stocks won’t have changed much. We expect volatility and shouldn’t over-react to it if we have a long-term view formed from (hopefully) unbiased analysis.

Disclaimer: This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. It does not contain financial advice. This article was supplied free to NBR and first published 16 August 2022.

Related reading

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

It is no secret that us New Zealanders love to invest in property as a way of building wealth. …

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

For investors that hold assets denominated in a foreign currency, there is a direct exposure…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…