Insights

The hunt for yield: expectations management

Published December 2025

Author:

Until the Reserve Bank of New Zealand’s (RBNZ) November monetary announcement, New Zealand interest rates had fallen to cycle lows. Indeed, over the last two years the average six-month term deposit rate fell from 6% in October 2023 to just 3.5% in October of this year.

While the official cash rate (OCR) is currently sitting at 2.25%, the yield curve – that is interest rates covering the periods beyond on-call to thirty years – is positively sloped; a function of market participants considering the next stage of the monetary policy cycle.

From a return perspective, with on-call and very shorted-dated deposits yielding lower returns than longer-term investments, there is a significant return opportunity cost associated with a typical cash deposit.

And it’s not only the low nominal or low headline return of a cash investment that should concern investors, don’t forget about the impact of inflation. Indeed, September’s annual inflation result was 3% therefore eroding the “real” return associated with very short-term investments.

What to do?

As always in investing, there is no-free-lunch. Simply extending the investment tenor to capture a higher return creates duration or interest rate sensitivity risk, which may deliver capital losses to investments made today, if term interest rates increase beyond current levels

However, as they say, all information is captured in the price – or yield – and efficient markets should guide investor decision-making.

In other words, do your homework. Let the facts guide you and let go of any deeply held opinions masqueraded as the facts.

With this in mind, we’ve recently heard a number of comments around fixed rate bond investments versus floating rate bond investments.

We’ll use a comparison between fixed rate corporate bonds (bonds that aren’t issued by a government) and corporate floating-rate bonds (also referred to as Floating Rate Notes, or FRNs) to illustrate our thinking.

Fixed versus Floating; you decide

We’re guessing most readers will be familiar with fixed-rated bonds - debt securities that pay a fixed coupon - which is calculated as the sum of the relevant wholesale term interest rate (think duration) and the issuer’s specific credit margin - until a set maturity date, at which time principal and the final coupon are be returned to the holder (assuming no default, of course!).

A Floating Rate Note is also a debt security with a set maturity date, but pays a coupon that is the sum of the issuer’s specific credit margin and a nominated, very short dated wholesale reference rate. In New Zealand this is commonly the very short duration one-month or three-month Bank Bills rate, that resets continually over the life of the floating rate note. The math is easy: a standard floating rate note that matures in three years’ time will have twelve 3-month rate-sets

The logic that has been presented to us is as follows; if interest rates are going higher then wouldn’t an investor be better off keeping duration short, taking the short-term pain of the opportunity cost and corrosive effects of inflation by preferring a floating rate note? On the basis that the floating rate note will be replaced with a fixed rate bond once yields have been determined to have peaked.

The logic seems defensible, but we first need to fully understand the relationship between wholesale term interest rates and shorter-term wholesale reference rates.

The fact of the matter is that wholesale term interest rates are simply the sum of the shorter- term wholesale reference rates. Add to this the specific issuer’s credit margin corporate – which should be the same for either a fixed rate bond or floating rate note – to get the coupon yield.

Indeed, we can solve for the yield of a 3-year wholesale interest rate by summing up the expected values of the associated twelve 3-month wholesale reference rates.

The table below shows the closing value of the 3- year wholesale term interest rate of 3.10% on 3 December 2025. This approximates to a simple average of the twelve 3-mth wholesale reference rates of 3.08% - this is a simplistic exercise but indicates that longer term rates already incorporate expectations of where shorter rates are expected to go.

Source: LSEG

Knowing this, if an investor had no view on where interest rates were going, they should be indifferent to investing in a 3-year fixed rate bond or a 3-year floating rate note.

Alternatively, armed with this information an investor can make an informed decision.

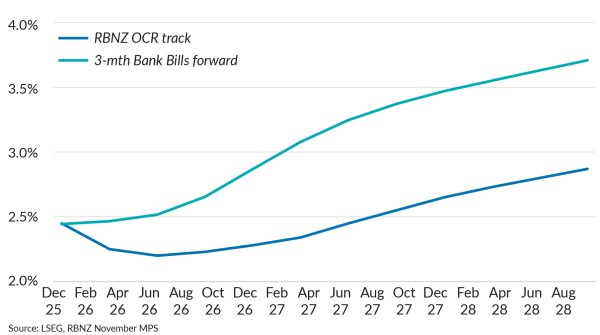

To us, the wholesale short term reference rates, or in this case the 3-month Bank Bills rates, look too high when compared to the forward track for the OCR published in the regulator’s November monetary policy statement.

We acknowledge that the 3-month BKBM rate and OCR are slightly different instruments but counter that when compared historically, observations are broadly consistent. The current difference is significant.

The table shows our interpretation of the market’s expectation for the 3-mth Bank Bills rate and the RBNZ’s forward OCR track.

We generally expect to term interest rates to move higher, but not as high as currently expected – not at this stage, anyway!

Liam Donnelly is an Equity Analyst and Assistant Portfolio Manager at Octagon Asset Management.

This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. This article does not contain financial advice. Some of the Octagon portfolios may own securities issued by companies mentioned in this article.

Octagon Asset Management is the investment manager for Octagon Investment Funds and the Summer KiwiSaver scheme.

Related reading

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

It is no secret that us New Zealanders love to invest in property as a way of building wealth. …

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

For investors that hold assets denominated in a foreign currency, there is a direct exposure…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatil…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…