Insights

Currency hedging: a financial markets free lunch?

Published May 2023

Author:

ANALYSIS: We can use currency hedging as a way to mitigate the risk associated with the currency exposure.

For investors that hold assets denominated in a foreign currency, there is a direct exposure to exchange rate risk, as well as the price risk of the international assets.

A New Zealand investor who buys shares in Amazon Inc – a US-listed stock, denominated in United States dollars (USD), has exposure not only to Amazon business profits but also movements of the New Zealand dollar (NZD) currency rate against the USD.

However, we can use currency hedging as a way to mitigate the risk associated with the currency exposure, with the idea of reducing the total investment risk and potentially improving risk-adjusted returns.

Hedging, as the name suggests, means that as one asset falls in value, movements in the other have the ability to compensate. To be an effective hedge, the movements in the two investments (foreign assets and the currency) need to move in opposite directions, known as negative correlation. If the correlation of the two assets is not always minus one, there will be times when the hedge does not work the way an investor would normally expect.

Currency movements are hard to forecast in the short term, however we believe the NZD is mean reverting around a moving trend (mean reversion is a financial term for the assumption that an asset’s price will tend to converge to the average price over time), based on the purchasing price parity of the NZD. The impact of currency on returns tends to decline over time as movements revert back to trend. On that basis, an investor could remain unhedged, knowing that, in the very long term, the impact of the currency on the value of offshore assets will be minor.

In this column, I’ll discuss some of the arguments for and against hedging portfolios of international shares in foreign currencies back to New Zealand dollars.

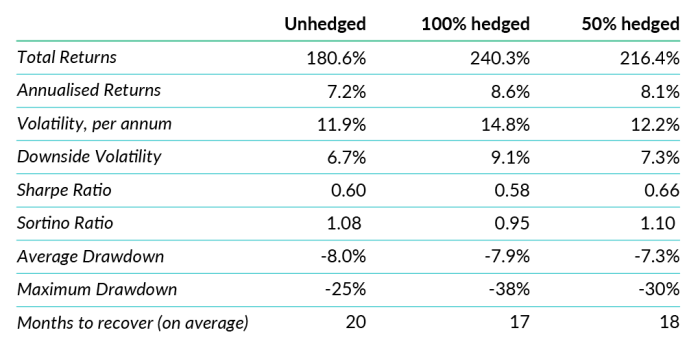

Currency heading impact on All Country World Index, of $100 base investments

Academic analysis

A 1988 paper by Perold and Schulman, in the Financial Analysts Journal, found that currency hedging greatly reduces risk with zero impact to return. Hedging is therefore a costless way to minimising portfolio risk and does indeed appear to be a ‘free lunch’.

When I review that work, using 15 years of historic NZD hedged returns of the MSCI All Country World Net Total Return Index (a broad-based global equity index), I find their conclusion is more nuanced.

Being hedged creates more risk than being unhedged, but this incremental risk comes with higher expected returns – a relationship that is reassuring and desirable. There is an upward trend in hedge-adjusted volatility – the more hedging you have, the more volatility you get, but it is not linear.

A 100% hedged portfolio delivers more return than an unhedged portfolio but at significantly higher levels of volatility and at a lower return for risk taken – we measure this in the Sharpe ratio.

We also see a higher maximum drawdown (the maximum loss from a peak to trough in a cycle), and the Sortino ratio (the additional return for each unit of downside risk) shows a 100% hedged portfolio sees a higher drawdown in periods of significant market stress.

The 50% hedged portfolio also delivers more return than an unhedged portfolio, and it also has a better return for risk, with a Sortino ratio in line with the unhedged position, a lower average drawdown and only a modest increase in maximum drawdown.

Portfolio construction

It is widely held that portfolio construction generally looks to maximise return for risk taken. However, a return-seeking investor may choose to be 100% hedged, chasing the extra return and accepting the higher volatility, even though this does not seem to be the ‘most efficient’ position to take.

Performances of hedged and unhedged portfolios of MSCI All Country World index

(From 2008 to 31 March 2023)

Sources: 1. Bloomberg; and 2. OAM analysis

In the equity market sell-off of 2011, hedged portfolios added returns and lowered volatility for the two years until investment markets recovered. However, in the market dislocation around the outbreak of Covid-19, a fully hedged portfolio did significantly worse than an unhedged portfolio for a period of time.

Interest rate differential

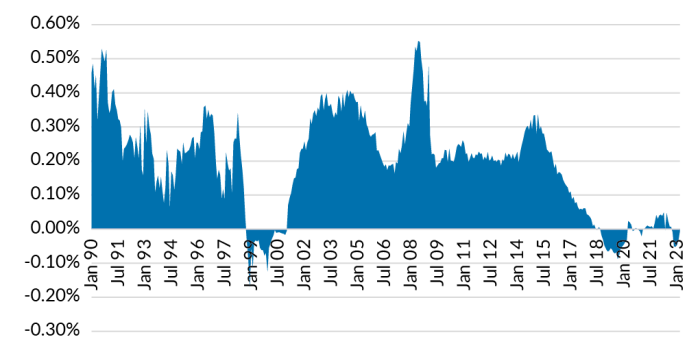

Additional factors to consider with hedging currency, other than minimal costs associated with transacting the hedge, are costs – or benefits – that come in the form of a ‘carry trade’ concept.

A positive carry trade generally means you can borrow in a low-interest rate currency to buy a currency where cash is earning a higher interest rate. It becomes a negative carry trade when we buy a low-interest rate currency with a more-expensive-interest rate currency.

The NZD has over the past three decades ‘earned’ mostly a positive carry trade against the USD. Why? Simply due to higher interest rates here in New Zealand than in the US.

Roughly speaking, the average per-month premium has been +0.14% or +1.7% in annual terms – courtesy of being able to transact at the lower US interest rate to enter into a NZD currency hedge at a higher domestic interest rate.

But we caution there are periods when the NZD interest premium has been negative.

Interest rate premiums have an impact on the hedged performance. These premiums are a by-product of a hedging strategy and, whether positive or negative, need to be considered in conjunction with greater or lesser risk.

Forward rate premium NZ and US, per month read from 1990 to 2023

Sources: 1. Bloomberg; and 2. OAM analysis

Within the context of a lower positive carry trade right now, we need to consider the right sizing of hedging positions, which is part of risk budgeting in portfolio construction.

As with all investment strategies, an investor should start with a view of what works and what doesn’t, and a view on what they are good at and not so good at. This can help offset behavioural biases and sets up a framework to objectively review how the strategy works through time.

Disclaimer: This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. It does not contain financial advice. This article was supplied free to NBR and first published 9 May 2023.

Related reading

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

It is no secret that us New Zealanders love to invest in property as a way of building wealth. …

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatil…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…