Insights

Asset rich, cash flow poor

Published October 2024

Author:

ANALYSIS: Synlait Milk is a case study for when asset backing is no longer enough to support valuation

It is no secret that us New Zealanders love to invest in property as a way of building wealth. For many mum and dad property investors the appeal is that the investment is a tangible asset that you can see and feel as opposed to the lack of tangibility of shares or investment funds.

These mum and dad investors are not alone in seeing this appeal, for decades investors into equity markets have used a company’s asset backing to support their view of valuation. This is typically done by using book value per share (BVPS) as an anchor point for fair value. Book value is the value of a company’s assets less their liabilities, in layman’s terms it represents the theoretical value shareholders would receive if the company was liquidated tomorrow.

In essence, BVPS is most useful as a valuation tool when a company largely uses tangible assets to derive their profits. Widely known as the father of value investing, Benjamin Graham popularised the concept that stocks trading below their BVPS were attractive investment opportunities as the net assets held by these companies offered a margin of safety and a low level of risk. Yet the disconnect of Synlait Milk’s (SML) share price from its historically strong relationship with its BVPS is evidence that this strategy is not always fruitful, begging the question – when is asset backing no longer enough to support valuation?

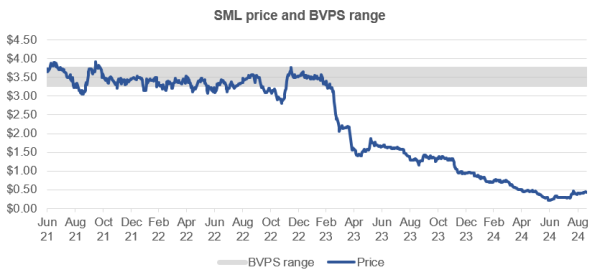

Just this month shareholders in Synlait voted to approve a $220 million recapitalisation by its two major shareholders A2 Milk (ATM) and Bright Dairy. Synlait had warned that failure to approve the recapitalisation would likely see the company cease trading and initiate a formal insolvency process. The below chart demonstrates that for some time Synlait’s share price bore a close relationship to its BVPS. This was largely due to the fact that book value was supported by its very real assets including its infant formula plant at Dunsandel; the Dairy works business; and its freshly built $450 million North Island assets with its Pokeno plant having signed a major customer to deliver volumes. For a time, these assets served to reassure investors of a valuation floor. So, what went wrong?

Source: Refinitiv, Synlait Annual Reports

Synlait’s share price and BVPS first began to materially disconnect in March 2023 when the company issued a whopping 58% downgrade to its FY23 NPAT guidance from a range of $45-50 million to $15-20 million. The two key drivers of that downgrade were reduced demand from A2 Milk at Dunsandel and another delay in the ramp up of volumes at Pokeno.

What has since followed in the last 18 months has been a continued downtrend in profitability with four further earnings downgrades to the point that ahead of the recapitalisation Synlait had to withdraw their FY24 guidance for EBITDA in the range of $45-60 million stating their expectations it would be below the bottom end of that range.

Just yesterday Synlait ended up printing an adjusted EBITDA of $45.2 million (versus a reported EBITDA of negative $4.1 million), a far cry from their initial guidance of FY24 EBITDA to be an improvement on FY23 (which was $90.7 million). At the same time earnings have cratered net debt has soared to $551 million, putting Synlait well in breach of their banking covenants and necessitating the recapitalisation.

You might now be recalling that a mere two paragraphs ago I said that when a company largely uses tangible assets to derive cash flows then BVPS can be a good measure of valuation support. Therein lies the problem for Synlait. What has become apparent over the last 18 months is that those assets no longer serve to act as an anchor to the share price because their value is not supported by another aspect crucial to intrinsic valuation – cash flows.

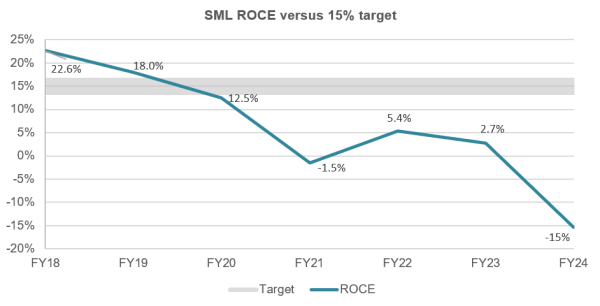

Not just any cash flows as well, cash flows that support sufficient returns on the millions of dollars of capital that have been invested into these assets. The chart below shows that the return on capital employed (ROCE) profile has deteriorated and sits well below Synlait’s target of 15%. This deterioration is mainly down to the lack of utilisation occurring at Pokeno. The plant has roughly 30kT of capacity. It was estimated that by now volumes would be sitting around 17kT as its signed customer, Abbott, continued to ramp up production. Today the reality is that Pokeno has 4kT of volumes going through it.

As a quick back of the envelope calculation, Synlait as of their FY24 results yesterday had a book value of $604 million. In applying a cost of capital of 12% to the business to reflect earnings uncertainty, Synlait would have to print an NPAT of roughly $73 million to produce a sufficient return on capital – FY24’s underlying NPAT was negative $60.4 million. All of this serves to show us that BVPS is not a sufficient view of valuation on its own – we need to dig deeper to understand the fundamentals behind a discount to BVPS.

Source: Synlait Annual Reports, FY24 to be updated

Today, Synlait trades around $0.38, while its BVPS is $2.76 (pre-recapitalisation movements). The disconnect tells us that something is wrong. Brave investors willing to back a turnaround in profitability might see this as an opportunity but will have to be patient. The recapitalisation may have saved Synlait from insolvency, but it also serves as evidence that these assets were valued too cheaply and 0.1x price-to-book might not be the right number. After all, Bright has supported the majority of the recapitalisation at a premium to TERP and it is no secret that a large part of A2 Milk’s $4 billion market cap is reliant on the SAMR licences attached to Synlait’s Dunsandel. The value of the assets is two-fold in asset utilisation and profitability, both which have question marks still surrounding them.

Whilst BVPS can still serve as an accompaniment to wider valuation methodologies, Synlait has reminded us of the consequences of focusing only on one indicator of value when we needed to dig deeper.

Paige Hennessy is an Equity Analyst at Octagon Asset Management

Disclaimer: This article has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. This article does not contain financial advice. Some of the Octagon portfolios own securities issued by companies mentioned in this article. Octagon Asset Management is the investment manager for Octagon Investment Funds and the Summer KiwiSaver scheme.

Related reading

CSL and Fisher & Paykel Healthcare (FPH) were working their…

At first glance, the recent surge in Briscoes’ share price might imply a significant earnings beat, takeover speculation, or p…

The last two or three years have seen the Official Cash Rate (OCR), and other short-term interest rates, touch heights not seen since before the …

Fittingly for an industry bu…

The past couple of years have been challenging for domestic bond investors. The Bloomberg N…

The core concept of Environmental, Social, and Governance (ESG) has existed for centuries, dating back to religious codes banning investments in slave labour, through to div…

Kiwi households have almost NZ$250 billion sitting in their bank accounts - that's more than double all of th…

For investors that hold assets denominated in a foreign currency, there is both a direct exposure to exchange rate risk, as well as the price risk of the a…

Octagon looks to enhance the returns for our customers by being an active manager in the markets we invest in. This means, by definition and sty…

Bonds are often seen as less glamorous, less volatile, and basically boring when compared with the high-octane, high-ris…

Diversification is the great free lunch in investing – a …

to streamline the post-election government formation process.

Waiting for Godot, by Irish playwright Samuel Beckett, is a tragicomedy in two act…

More than a half-century ago, in November 1971, the then Prime Minister of New Zealand Keith Holyoake flew to Invercarg…

Say we flip a coin. Heads or tails? Heads – you may carry on exactly as you are now. Tails – 77% of your revenue strea…

How profitable are New Zealand’s banks? Seems a fair question aft…

For investors that hold assets denominated in a foreign currency, there is a direct exposure…

In a July 2022 article we covered the basics of New Zealand Government inflation-linked bonds; how the…

A paper by the International Monetary Fund titled ‘The Long-Run Behaviour of Commodity Prices:…

With its mild weather, beautiful beaches, bountiful natural resources, and economic performance, Australia is often described as the lucky country (…

The term ESG (Environmental, Social and Governance) was officially coined in a 2…

New Zealand net migration has been a hot topic of late. As our econo…

One of the simplest truisms in investing is that share prices follow profits – on average, over the long term. Perh…

A few years back I read a book by Daniel Kahneman, Thinking Fast and Slow. It coined a phrase that captures the way I think about volatil…

Inflation-linked bonds are another option for income investors.

Today, we’re going to discuss wha…

The effects of Covid continue to reverberate throughout New Zealand more than two years after…

Where we came from

The boom in New Zealand’s property market has been extremely…